09. Fama French Risk Model

M4 L2A 20 Fama French Risk Model V3

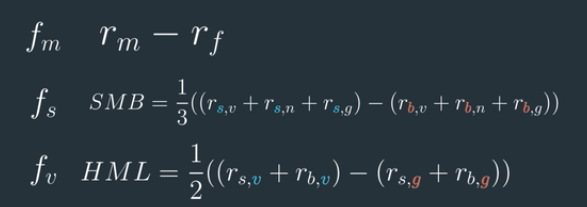

Matrix of Factor Returns

Calculate the covariance matrix using the time series of factor returns.

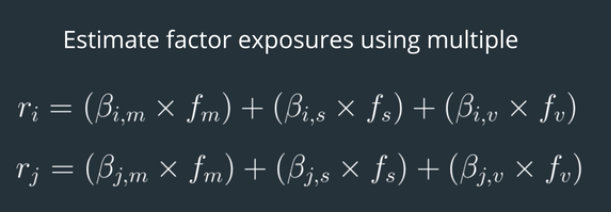

Matrix of Factor Exposures

Use a multiple regression to estimate the factor exposures.

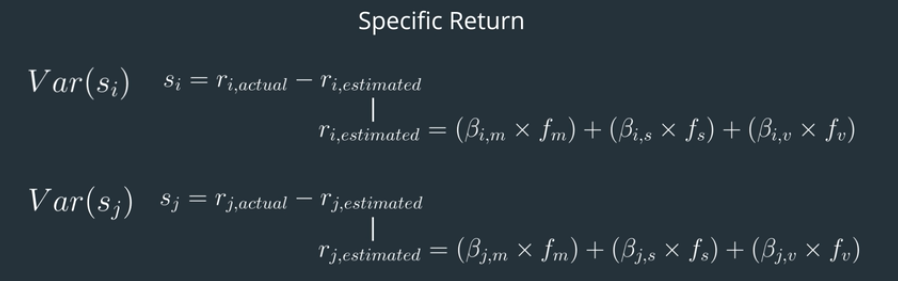

Specific Variance

Calculate the actual minus estimated returns as the specific return. The variance of that time series is an estimate of specific variance.